Cementing its Turnaround

Can you find a good company in a seemingly bad industry?

Today’s article is not about AI, data centers, power systems, or oil and gas. This is a company suffering from a multi-year industry decline. The first question may be: why bother at all? Why not pick companies in fast-growing industries?

The answer: This company is quietly turning itself around by aggressively diversifying overseas. Although it sells practically the same cement products globally, the prices, margins, and demand overseas are multiples of those in China. In addition, the Chinese market could potentially recover if enough overcapacity is cut.

The financials are showing signs of a turnaround for the first half of 2025:

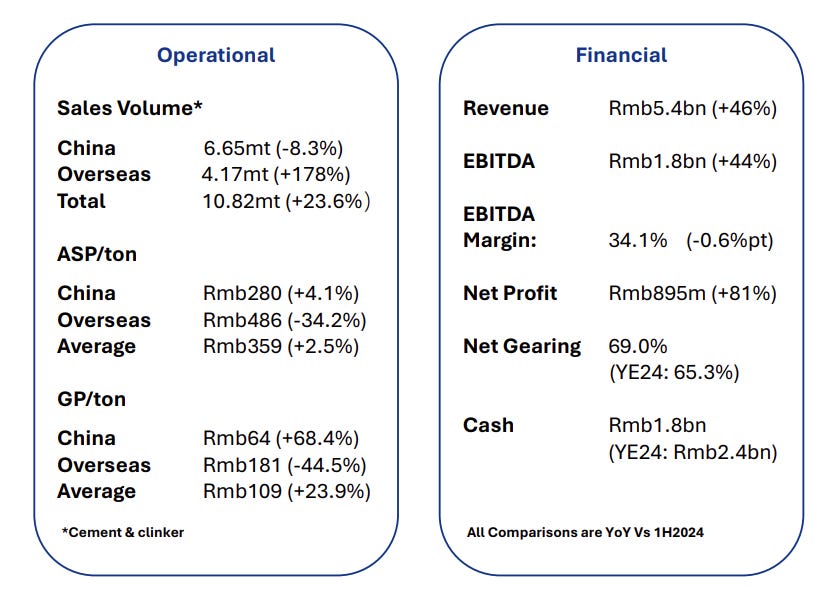

Revenue: +46% yoy

EBITDA: +44% yoy

Net profit: +81% yoy

On an annualized basis, this company is trading at 14x P/E and 7x EBITDA.

Let’s dive in!

Before we dive in: This is not investment advice. Please do your own research. And if you would like to comment, please be respectful to capybaras; they deserve it.

Introducing West China Cement

West China Cement (WCC) (HKEX: 2233) is a leading cement producer in Shaanxi Province, China. It has a leading market position in Southern and Eastern-Central Shaaxi. From a standing start in 2020, WCC has been expanding in Sub-Saharan Africa and Central Asia, with production capacities in Ethiopia, Mozambique, the Democratic Republic of Congo (the ‘‘DRC’’), Rwanda, Tanzania, and Uzbekistan. Uganda and South Africa will soon be added to this list.

WCC had a busy 2025:

Overseas growth

DRC: Announced acquisition of Cimenterie de Lukala SA (CILU) in Jan/25, an integrated cement plant in Lukala, the capital city of the DRC. The transaction closed in late 2025.

Uganda: Just last week, the construction of its Uganda production facility was completed, adding 3m tons of cement capacity.

South Africa: announced acquisition of AfriSam, a major South African cement producer with 4.5m tons of capacity.

Mozambique: A 1.5m ton project will begin construction in 2026.

Kazakhstan: 2m project began construction in Oct/25.

Divestment: In Aug/25, it completed the disposal of its Xinjiang cement plant, totaling 3.5m tons. Proceeds used to 1) partially repay the Group’s US$600 million 4.95% senior notes due in Jul/26 and 2) invest overseas.

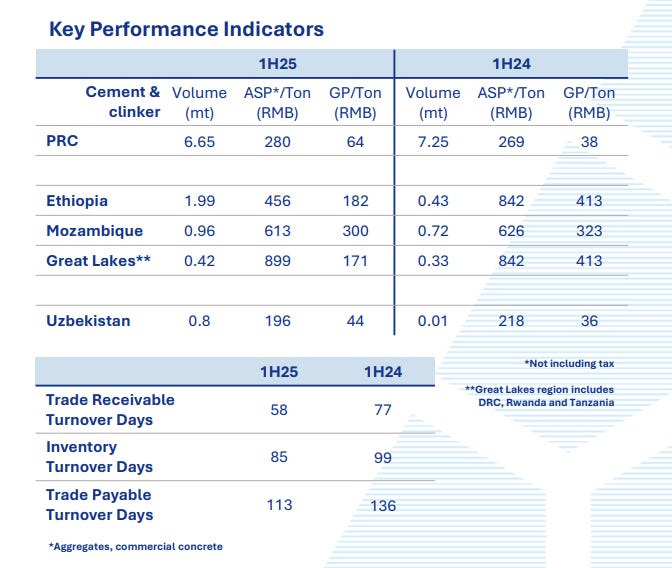

Here is the company’s cement production capacity breakdown as of 1H25:

China: 25m tons (post Xinjiang disposal).

Overseas: 13.6m tons (14.8m post CILU acquisition).

As of Jan/26: 17.8m tons capacity post CILU acquisition and Uganda plant completion.

2027E capacity: 25.8m tons after the closing of the AfriSam deal and the construction of the Mozambique and Kazakhstan plants.

All presentation slides are from West China Cement’s 2025 Interim Results Presentation

Industry Overview

To analyze West China Cement, we need to have an understanding of cement demand trends in both China and the respective countries in Africa.

In China, cement demand is driven by the construction market. The construction market is made up of real estate and infrastructure investments.

Real Estate Development Investment (RDI): In 2024 and 1H 2025, Shaanxi’s RDI increased by 0.5% and 0.9%, compared to China’s -10.6% and -11.2%.

Fixed Asset Investment (FDI): In 2024 and 1H 2025, Shaanxi’s FDI grew 5.2% and 5.6%, compared to China’s 3.2% and 2.8%.

Despite outperforming the rest of the country, cement demand in Shaaxi remained lackluster. Demand is supported by government infrastructure projects, such as the Xi’an to Shiyan and the Xi’an to Ankang to Chongqing High Speed Railways, as well as numerous reservoirs and water projects, hydro power projects, highways, and gas transmission projects. Under the “Outline for National Comprehensive Transport Network Planning”, China designated Xi’an as a core city in the Silk Road Economic Belt development and to be developed as a hub for international transport, including freight and railway, between 2021 and 2035. Due to China’s declining population and the ongoing troubles in real estate, FDI will be the key indicator to monitor.

Oversupply: Lower cement demand is causing WCC and its competitors to adopt supply-control policies, such as seasonal production halts, increasingly stringent environmental controls, and the closure of older, less efficient capacity. This has escalated to the national level, with the PRC government announcing various anti-involution (反內卷) policies to reduce overcapacity in key industries, including the cement industry. The State Council introduced policies limiting production capacity, production controls, low-carbon targets, and capacity upgrades to reduce capacity.

As for West China Cement’s African operations, the industry tailwinds are much stronger.

Population: Africa has the world’s fastest-growing population. In 2024, 1.5 billion people lived in Africa. This is expected to increase to 2.5 billion by 2050. 26% of the world’s population will be in Africa by 2050. This population will need to be supported by infrastructure development and urbanization.

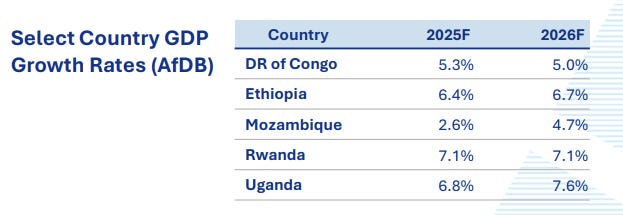

GDP growth: Africa has some of the fastest GDP growth rates in the world. GDP growth is expected to accelerate to 4.1% and 4.4% in 2025 and 2026. In 2025, it is projected that 12 of the world’s fastest-growing economies will be in Africa and East Africa, where WCC’s operations are located. They will grow by over 6% in 2026.

Cement per capita: Sub-Saharan Africa has some of the lowest per capita cement consumption rates in the world at lower than 100kg per annum. This is less than 10% of China’s per capita numbers and less than one-third of the global average.

China’s Integration: Aided by the Belt and Road Initiative, China is not just investing in cement production but also in infrastructure development.

Here is a brief overview of West China Cement’s country exposures

Ethiopia: Largest overseas operations. Entered in 2022 through the acquisition of the 1.3m ton National Cement Plant. Commissioned a 5m ton plant in Sep/24, one of the largest cement production lines in Africa. Ethiopia’s GDP growth rate is around 6%. Cement demand is led by infrastructure (roads, rails, airports) and is expected to reach 13m tons in 2025, while supply is 10m tons. FX restrictions were gradually eased in 2024 as part of the country’s reforms. An IMF financing package and outward remittance of dividends are expected in 2H 2025.

Mozambique: First entry into Sub-Saharan Africa. Commissioned a 2m ton plant in Dec/20, one of the country’s two operational plants. GDP growth rate of around 4%. Cement demand of 3.5m tons, with supply at 2.5m tons. Long-term cement demand growth includes the development of large liquefied natural gas resources. Mozambique experienced political conflict in Q3/24, but this subsided in early 2025. Since then, the country has seen record construction activity and cement demand.

Great Lakes Region (Rwanda, Tanzania, DRC): 5-7% GDP growth. Cement demand in the DRC is around 4m tons in 2025, while supply is 3m tons. High FDI growth, but ongoing conflicts are creating difficulties in transporting cement.

Uzbekistan: 5% GDP growth until 2030. Several large-scale infrastructure projects, including the China-Kyrgyzstan-Uzbekistan Railway, extensive road construction, and over 3,000 mini hydro power stations, are leading to projected cement demand growth rates of 15%. However, the industry is in oversupply due to new capacity from WCC and Anhui Conch Cement. Old capacity is being shut down, and the government suspended new capacity approvals.

Uganda (new operation in Jan/26): 6-7% GDP growth in 2025, driven by oil production and pipeline construction. No currency controls, and a large mismatch between supply (1.24m tons) and demand (5m tons). A new 3m tons cement plant commenced operations on Jan 17, 2026, meeting not just domestic demand but also export markets such as South Sudan, DRC, and Kenya. According to new reports, this plant is expected to generate annual revenue of US$400m, or around RMB$2.8b, approximately 25% of annualized 1H25 revenue (or 33% of FY24 revenue)

Key Metrics - Operational

China: ASP stabilized from supply-side discipline, Gross Profit per Ton (GP/T) increased 68% due to lower coat cost. Utilization at Central Shaanxi was just 36%, although it was 70% at Southern Shaanxi. While the property development market remains weak, the infrastructure market is relatively active in Southern Shaanxi, with a few High Speed Railway projects and water projects underway.

Overseas: Large increase in sales volumes, resulting in a more reasonable ASP and GP/T. Expects overseas to become a greater proportion of WCC’s operations

Overseas revenue: 15%, 31%, 38%, 43% of total revenue from 2022, 2023, 2024, and 1H25

Overseas sales volume: 8%, 15%, 20%, 39% from 2022, 2023, 2024, and 1H25

Overseas gross profit: 28%, 53%, 67%, 58% from 2022, 2023, 2024, and 1H25

Shareholder Base

Zhang Jimin: 32% ownership. Chairman and founder of the company. He has 28 years of experience in the cement industry. He is also Chairman of the Shaanxi Province Cement Association, leading the association to formulate a self-regulatory regime, maintaining fair market competition, providing technology and human resources and assisting the Shaanxi Government in regulating the cement industry in Shaanxi Province.

Anhui Conch Cement: 29% ownership. It is one of China’s largest cement producers. Anhui Conch Cement invested in WCC in 2015 to gain exposure to Western China. WCC sold its Xinjiang plant to Anhui to diversify overseas.

Outlook

Continued overseas development: With the ongoing acquisitions and cement plant construction, overseas operations will continue to be the main focus. In 2027, overseas capacity will be more than 50% of the Group’s total capacity. I expect overseas gross profits to exceed 70% of total gross profits in the near future, absent an unexpected improvement trajectory in China.

China's recovery? China's cement production decreased by 7% in 2025 to 1.69b tons. Overall utilization was only 50%. Although ASP decreased in 2H 2025, coal prices declined even more. We may see improved profitability from domestic cement producers for 2025. Only 6m tons of new capacity was added, a 40% decrease yoy.

Risks

Political instability and FX controls: Unpredictable in Africa. Will China continue to be welcomed as a foreign investor? Will the Belt and Road Initiative be favored?

China’s supply-side discipline: Anti-involution policies, producer discipline, ASP, and coal prices.

Anhui Conch relationship: Anhui Conch is owned by the Anhui government. How swift is the decision-making process at the WCC level? Do they need to report to the Anhui government? Will Anhui compete against West China for African assets?

Thank You For Reading!

Hope you enjoyed the article. Please share, comment, subscribe, or pledge your support by donating to this page if you find it interesting!

Feel free to leave a comment on X as well! @capytalmgmt

Good article