Is This Happening Again?

Can a stock still be undervalued after a 4x?

Today’s article is an updated view of one of my best friends (stocks). I wrote about this company a few times. Its name is Tenaz Energy (TNZ).

Looking at this chart below without the ticker, you might have thought I copied and pasted Nvidia’s 5-year stock price.

That is not the case.

This chart is the 5-year performance of Tenaz Energy, a Canadian-listed oil and gas company, with the majority of its assets sitting in the Dutch North Sea, producing TTF natural gas.

Before we dive in: This is not investment advice. Please do your own research. And if you would like to comment, please be respectful to capybaras; they deserve it.

All of the presentation slides below are from Tenaz’s Corporate Presentations

Tenaz Brief Review

For those who are unfamiliar with their story, please kindly visit the following posts. I was far from the first to notice Tenaz, but I gladly picked up shares at $7 (dollar amounts in CAD unless otherwise noted) after the NOBV announcement.

Post #1: Tenaz as a special-situations investment, driven by its masterful NOBV acquisition at 1x FCF.

Post #2: Major updates include receiving government approval for the NOBV deal and raising $140m of debt as dry powder.

Post #3: Revisiting Tenaz after a 30% drawdown, with my thesis changing from a special situation company to a value-oriented investment with a capable management team and a proper strategy.

Post #4: I also briefly mentioned Tenaz in my 1H25 portfolio update. They successfully closed the NOBV deal and received EUR$15m as part of the deal arrangement. High TTF prices played a role, but the purchase price was ultimately the determining factor. Tenaz spent $22m buying an asset with $1b of reported (understated) reserves and ample exploration and development opportunities.

Exited My Position

Capytal Management decided to sell at around $18 a share because:

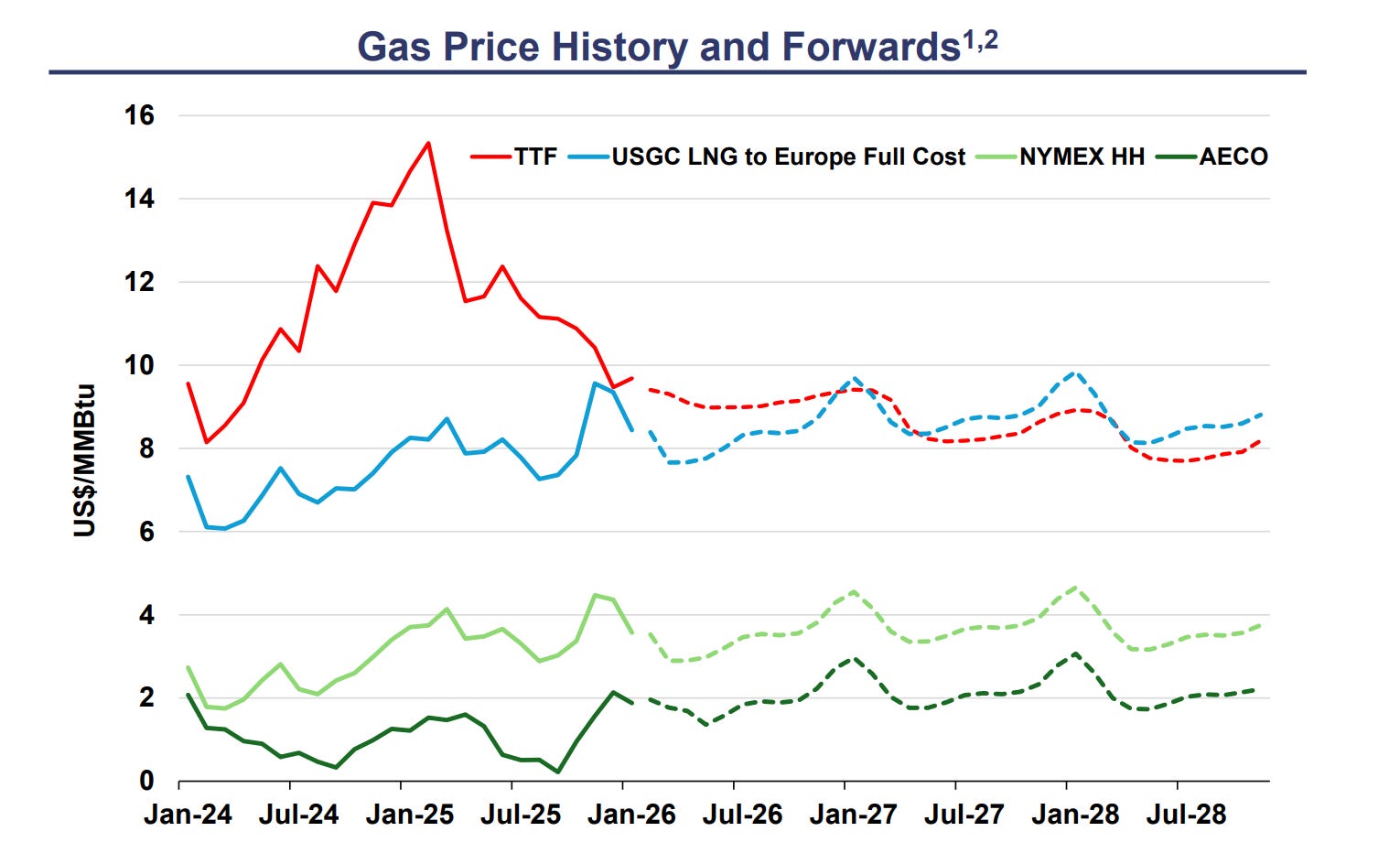

TTF: European natural gas prices have been trending downwards since Feb/25.

Better opportunities elsewhere: True to an extent, with some of the funds directed to Andean Precious Metals, Serabi Gold, NBIS, and PSIX. Of course, some went to losers such as TSSI and Kwan Yong.

Near-term cash flow drain: NOBV’s reinvestment opportunities are terrific, but the assets were underinvested for many years. I thought the near-term cash flow profile would be weaker given the high capital expenditures, which would take the market some time to realize its reserve development potential.

What Happened After I Sold?

GEMS Acquisition: Tenaz bought another attractive asset in the Dutch North Sea called GEMS. GEMS is operated by ONE-Dyas, the largest private oil and gas company in the Netherlands. Here are some of the key terms of the deal

Target assets: Natural gas assets at the Dutch and German sections of the North Sea.

Purchase price: $339m, plus $83m contingent considerations based on future reserve discoveries.

Funding source: $323m in cash, including $179m of new bonds issued at a 8.4% premium to par, 12% coupon (9.5% yield to maturity). $17m through equity issuance.

New facility: undrawn Reserve-Based Lending Facility with National Bank of Canada, CIBC, and Goldman Sachs.

Rationale

Low purchase multiple: 2.1x 2026E FFO, continuing its low-multiple + operational improvement M&A model.

Immediate per-share accretion: +31% production per share, +23% 2P reserves per share, +45% FFO per share.

High return on investment: <3 year payback period.

Manageable leverage: Net debt-to-EBITDA (2026E) at 0.9x post-acquisition.

Significant growth potential: GEMS production to grow from 3,200 boe/d in 2025 to 7,000 boe/d in 2026 and 12,000 boe/d in 2027, limited by current capacity. On a company-wide basis: 16,000 boe/d → 22,000 boe/d → 30,000 boe/d pro-forma net to TNZ from 2025-2027.

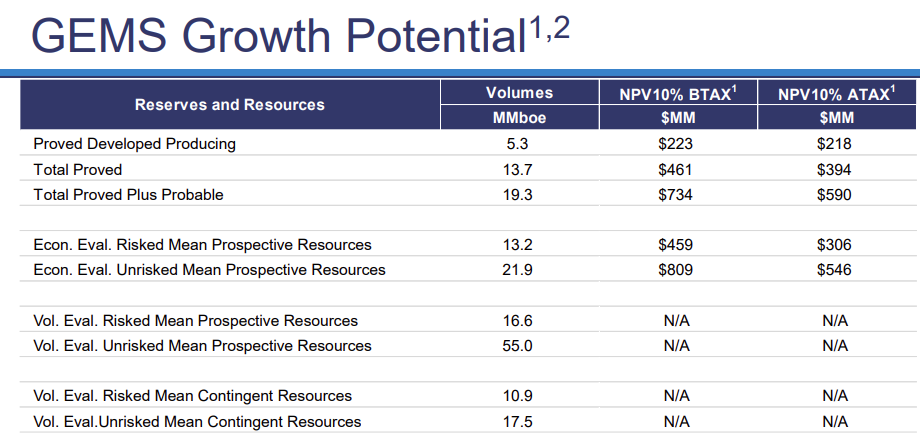

Lots of undeveloped reserves: Check the Prospective Resources in the presentation below; there is lots of upside to be captured.

We should expect an updated reserve report after FY 2025 results.

Management interest alignment: As part of TNZ’s 2021 recapitalization, the management team received warrants (exercise price: $1.80) and stock options (exercise price: $2.70) with an expiry date of 2026. The directors and officers have retained 70% of the shares from the exercised warrants and stock options, increasing their aggregate ownership of issued and outstanding shares from 11.0% to 16.3%. The remaining 30% was sold to fund applicable taxes and the exercise of the warrants and stock options. Their press release specifically stated they wanted to illustrate continued interest alignment with shareholders. To me, this is the biggest reason I decided to invest again.

National Bank $52 target price: National Bank expects Tenaz’s FCF and margins to expand meaningfully in 2027. Assuming flat TTF, the bank expects 25% FCF yield and TNZ’s FFO multiple compressing to 2.1x in 2027 (at $52!).

Risks

TTF Prices

One of my biggest worries leading to my TNZ exit was the impact of liquified natural gas (LNG) on TTF prices. I thought the US would flood European markets with LNG. However, Tony Marino, Tenaz’s CEO, made a few interesting points:

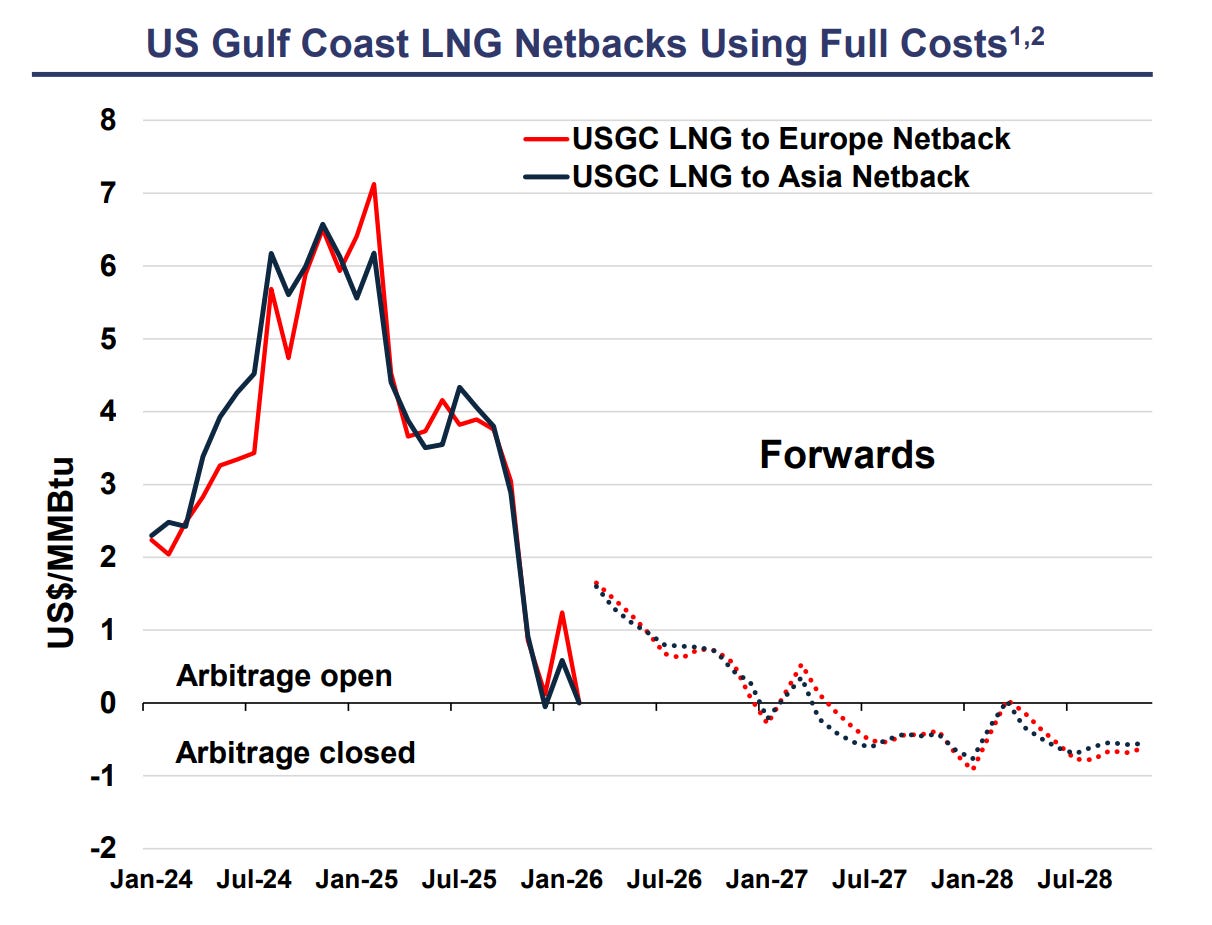

Negative netbacks: For LNG to be transported from the US to Europe, a number of expenses such as feedgas, tolling, liquefaction, vessel, and regasification must be incurred. Given the strong rally in US Henry Hub prices (driven by higher natural gas demand for electricity production), rising vessel fees, and lower TTF prices, netbacks (gas selling price minus operating expenses) are declining. According to the latest forward prices, netbacks are actually negative, disincentivizing US LNG exports. If netbacks remain negative for an extended period of time, it may delay long-term LNG plant buildouts.

Gas demand: Global gas demand is growing with greater visibility, unlike oil, driven by Asia’s economic growth, coal-to-gas/oil-to-gas switch, and AI data centers in North America.

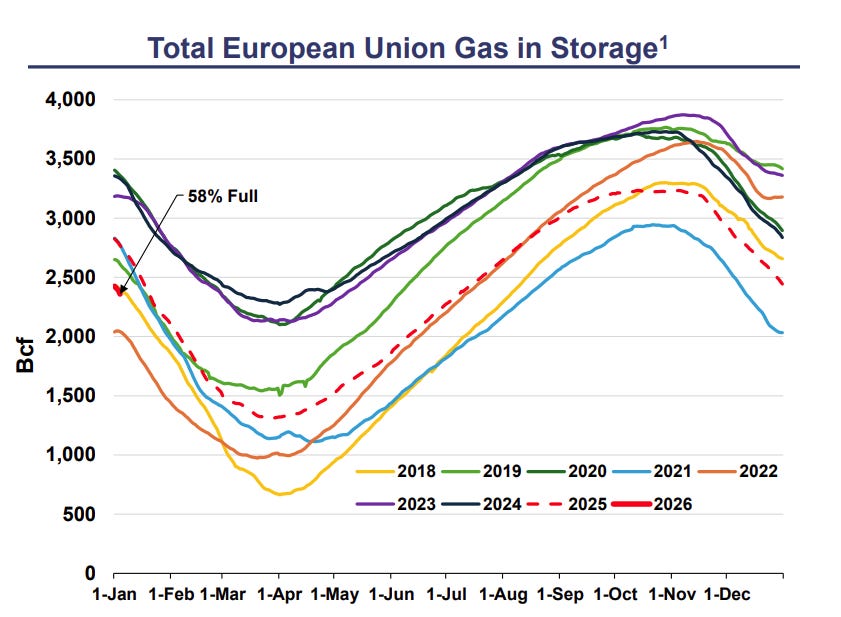

Storage: Lower than prior years

Hedging: even if TTF prices don’t stabilize as expected, the company is prepared through hedges. TTF price exposure is 56% hedged in Q4 2025, 43% in 2026, and 14% in 2027, using fixed-price instruments and collars.

Reinvestment Opportunities in the Dutch North Sea

As TNZ proved, there are ample targets in the Dutch North Sea with exploration and development potential. Eni’s natural gas assets could be next, solidifying TNZ’s position as the largest natural gas producer in the region. Even without a new asset, TNZ has enough assets on hand for significant organic growth in the coming years.

Capital Markets For Fossil Fuels

I thought Tenaz’s 12% coupon bond was a bit expensive, and they might have to continue to rely on high-cost, high-yield funding for future deals that might not be as economically attractive as NOBV. Their latest bond was issued at a 9.5% YTM, a lower cost issuance that proved markets like their strategy. I believe their next issuance would be at an even lower cost.

Thank You For Reading!

Hope you enjoyed the article. Please share, comment, subscribe, or pledge your support by donating to this page if you find it interesting!

Feel free to leave a comment on X as well! @capytalmgmt

So we buying this again or what captain?